Specific Identification Inventory Method Definition for Manufacturing

What is the Specific Identification Inventory Method?

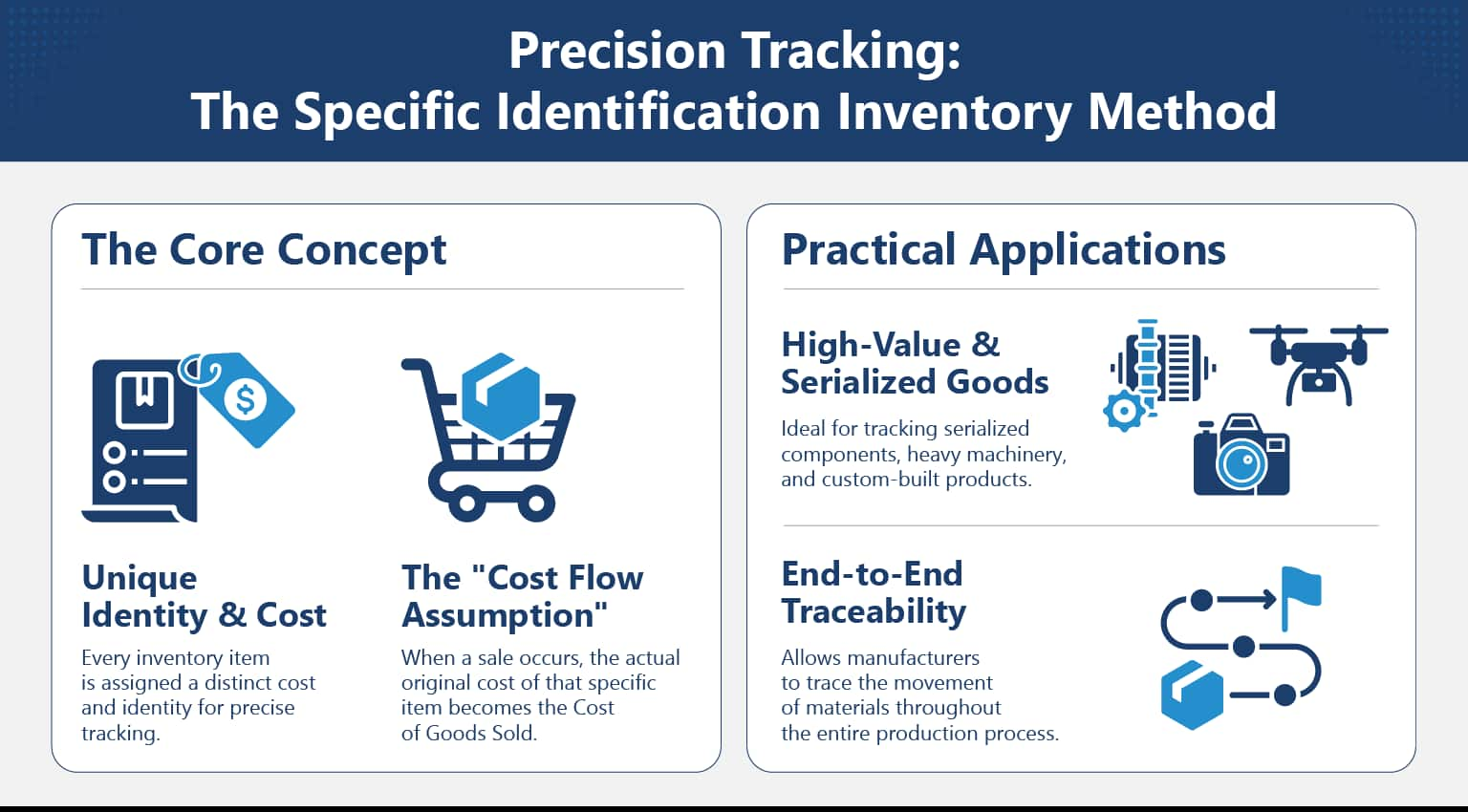

The definition of a specific identification inventory method is an accounting and tracking approach where each individual item in inventory is assigned a unique cost and identity, allowing that exact cost to be matched when the item is sold or used.

This means that each manufactured item, whether it be a:

- Serialized component

- Machine

- Custom-built product

can be traced back to its original cost and the movement of materials throughout the manufacturing process.

Where Does It Fit In Manufacturing?

4 Manufacturing Environments

This method is most appropriate in manufacturing environments where individual units differ significantly in cost or configuration. Symptoms of such environments include:

- Inventory items are unique or custom-built

- Unit costs vary substantially

- Production volumes are low to moderate

- Traceability of inventory is required for regulatory compliance or product quality.

4 Types of Production

The following production types favor the specific identification inventory method:

- Engineer-to-order (ETO) production

- Make-to-order (MTO) production

- High-value asset production (like industrial equipment, vehicles)

- Regulated industries requiring traceability

Where It Doesn’t Make Sense

This method is less practical for high-volume, low-cost manufacturing operations, where tracking each unit individually would add unnecessary complexity.

Which manufacturing systems are involved?

Within the context of a larger manufacturing system, the specific identification inventory method supports the functionality of:

- ERP systems: Where financial costing and inventory valuation occur at the unit level.

- MES system: Which track the production history, serial numbers, and movement through the manufacturing process of each item.

- Quality and compliance processes: Where the traceability of materials and components is required.

3 Benefits of Specific Identification

According to Pearson, the specific identification method “allows companies to accurately value unique or easily identifiable inventory items.”

The main reasons manufacturers choose the specific identification method include:

1. Accurate cost tracking

Producers can obtain an accurate view of the total cost of each item produced. This is particularly important when:

- Material costs vary drastically between units

- Custom configurations change production costs

- Labor and overhead differ by job or batch

Averaging product costs can distort margins and misrepresent profitability.

2. Improved traceability and compliance

For companies operating in regulated industries, the ability to provide a complete product genealogy, from raw materials through final production, is vital.

Specific identification enables:

- Full genealogy tracking

- Quick and efficient recall / problem resolution

- Regulatory compliance with industry standards

Without this method, manufacturers may struggle to identify defect sources or meet audit requirements.

3. Better Decision Making

Accurate unit-level costing improves:

- Pricing strategies

- Profitability analysis

- Customer and product-level insights

Without this method, blended costing can hide inefficiencies and reduce decision-making accuracy.

4 Step Specific Identification Process

Step 1: Assigning unique identifiers

Each item is assigned a unique identifier, such as:

- Serial number

- Lot number

- Asset ID

This identifier will connect the physical item to both the cost of that item and the historical background of that item.

Step 2: Capturing unit costs

Each time an inventory item is acquired, all associated costs are tracked.

Here is the type of cost that is often tracked:

- Labor costs

- Raw materials

- Overhead

For example, two products built from different materials may have a similar look and functionality, but they can have a very different unit cost.

Step 3: Tracking movement through production

As inventory moves through production and shipping:

- The MES system will document the production event.

- The ERP system will then update your inventory value to include the new information.

Each transaction is connected to the specific item rather than the overall inventory total.

Step 4: Match the cost at sale or usage

At the time you sell or use the item, the specific cost that was incurred by that exact unit will be added to your COGS (Cost of Goods Sold).

Similar to purchasing artwork, profitability is determined using the exact cost of the individual item rather than an averaged cost.

Specific Identification Inventory Method vs. FIFO

Specific identification maintains an individual record of the cost of each unit.

FIFO (First-In-First-Out) assumes the oldest inventory is used first.

Benefits of FIFO

FIFO is easier to use and is often less expensive than specific identification. However, it also does not reflect the cost of a specific unit of inventory as accurately.

Benefits of Specific identification

On the other hand, specific identification allows for precise matching of costs; however, it requires additional information to be tracked.

Specific Identification Inventory Method vs Weighted Average

Weighted average provides an average cost per unit based on both the quantity purchased and the cost of those purchases.

Specific identification retains the cost per unit for each inventory item.

Benefits of Weighted Average

Weighted average is simpler and less expensive to implement; however, it is less precise.

Benefits of Specific identification

Conversely, specific identification is more precise, but it is operationally more intensive.